US Treasuries

- 1st daily support is 4.43/4.44 73% to hold

- 2nd daily support is 4.455/4.465 75% to hold

- 1st weekly support at 4.435/4.465

- 2nd weekly support at 4.59/4.605 71% to hold

- 1st daily resistance is 4.335/4.35 50% to hold

- 2nd daily resistance is 4.30/4.31 90% to hold

- 1st weekly resistance at 4.30/4.32 54% to hold

Fed’s Waller: Cautious on Oil, May Advocate for Rate Cuts Later

Fed’s Bowman: Still Projecting Three Interest-Rate Cuts Before Year-End

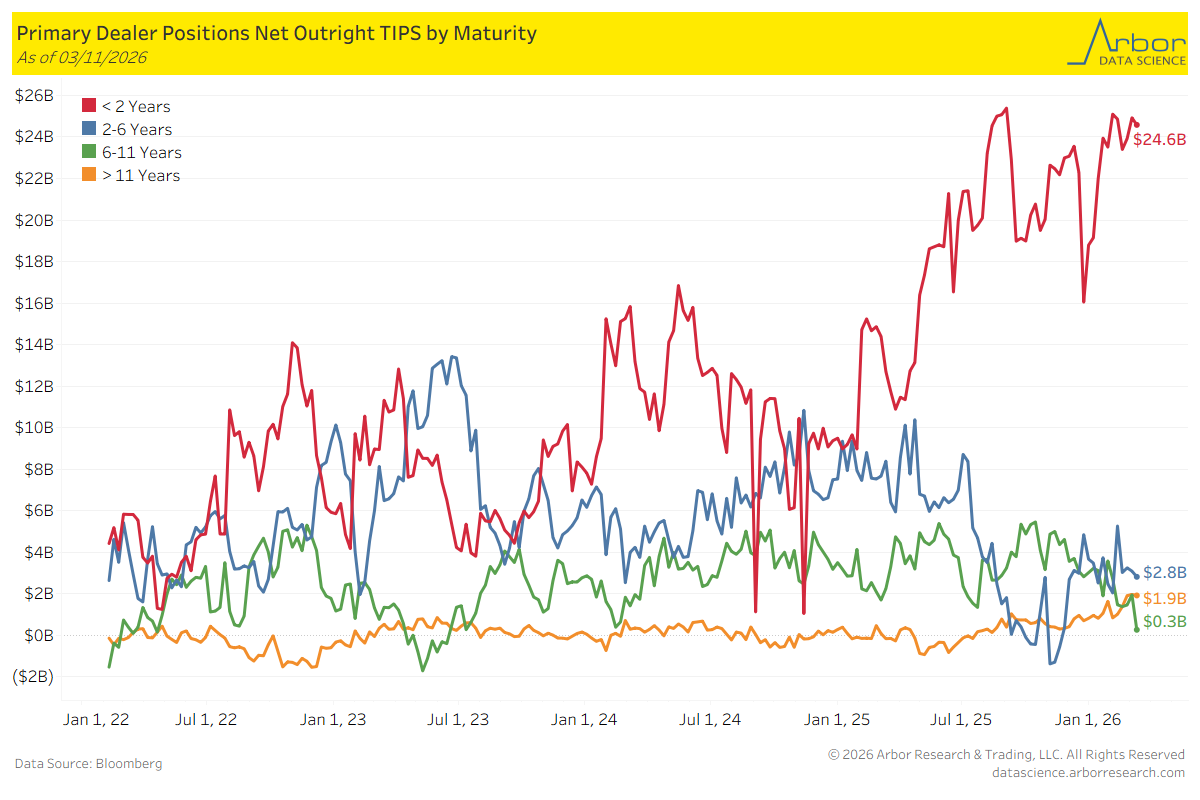

TIPS by Maturity (data through 3/11/2026)

Week over Week Changes by Maturity

- < 2 years: $24.9 Bn on 3/04/2026 to $24.6 Bn on 3/11/2026 = ($0.3 Bn)

- 2 – 6 years: $3.1 Bn on 3/04/2026 to $2.8 Bn on 3/11/2026 = ($0.3 Bn)

- 6 – 11 years: $1.9 Bn on 3/04/2026 to $0.3 Bn on 3/11/2026= ($1.6 Bn)

- > 11 years: $2.0 Bn on 3/04/2026 to $1.9 Bn on 3/11/2026 = ($0.1 Bn)

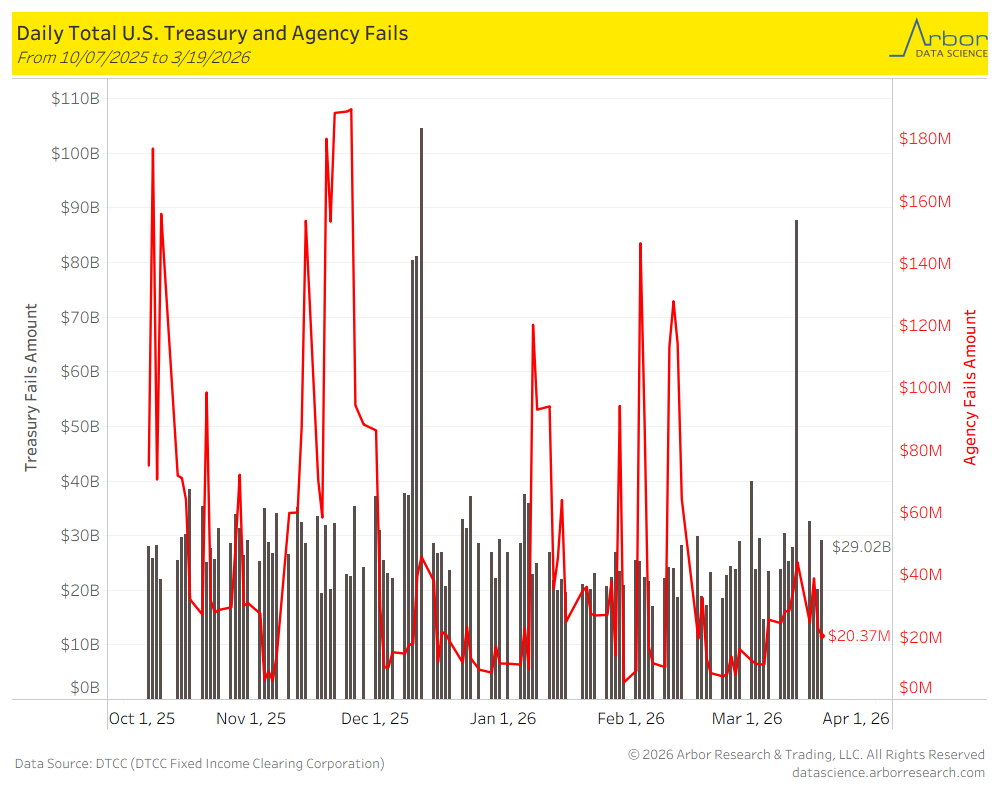

US Treasury Trade Fails

As of 3/19/2026, U.S. Treasury Fails were $29.02 billion and U.S. Agency Fails were $20.37 million.

Intraday Commentary From Jim Bianco

*SPAIN ANNOUNCES €5B AID PACKAGE TO CURB IRAN WAR IMPACT

This package includes suspending petrol taxes. I understand the sentiment, but as I argued in the conference call yesterday, the world is short 10 to 15 million barrels of crude oil. So, the world needs to consume 10 to 15 million barrels less. This is done by raising the price to shut out the marginal buyer (who can no longer afford it), resulting in 10 to 15 million fewer barrels consumed.

If Spain, or anyone else, is going to subsidize the higher price (by cutting taxes), then consumption will continue at the same pace. This means the price has to go even higher to shut out those marginal buyers. The fix is to open the Strait and get the oil flowing, not subsidizing higher prices.

Maria Bartiromo on X: Treasury Secretary Bessent unveils plan to flood market with oil amid Iran war

Bessent announced yesterday that the administration is thinking of “unsanctioning the ~140 million barrels of Iranian oil on the water.”

Way too many people think this changes something. It does not. If anything, it makes it worse.

—

Iranian oil has been sanctioned for many years. The 140 million barrels he is referring to are part of the “dark fleet” that has been shipping Iranian oil to Asia (mainly China) for years. Iran gets money for oil, and China buys it at a discount. So, this oil already exists in the world market. It doesn’t matter who buys it, or under what scheme (sanctioned through a dark fleet or legitimate open market sale), as a barrel sold anywhere, for whatever reason, adds to world supply.

To emphasize, these barrels are already part of the world supply. These barrels are not randomly floating in a tanker on some ocean (for years?), waiting for sanctions to be lifted before they can be sold and offloaded. By allowing oil to be unsanctioned, all Bessent is doing is allowing Iranian oil to be sold to places like Japan or South Korea. In other words, all he did was raise the price of Iranian oil because they now have more bidders.

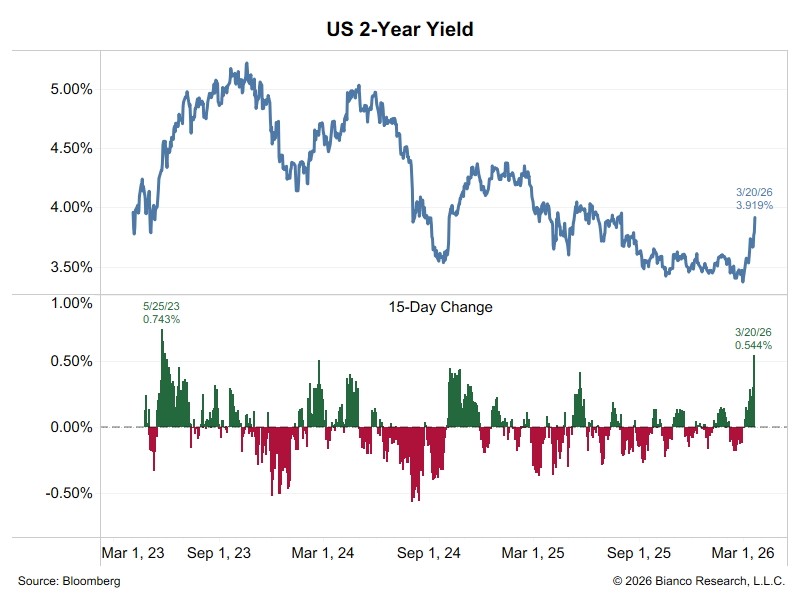

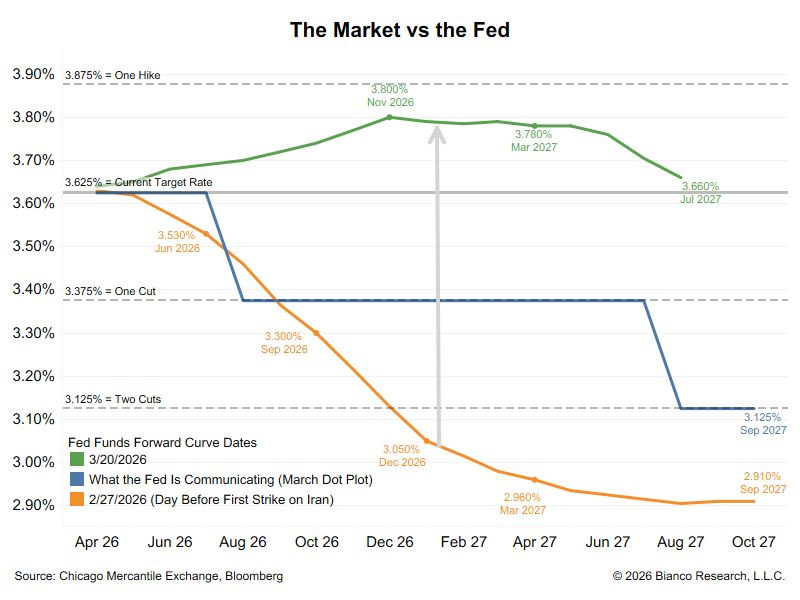

The war started three weeks ago (15 trading days). The 2-year is now up 54.4 bps over this period.

The biggest such rise in yields in three years (when the Fed restarted hiking after the SVB failure).

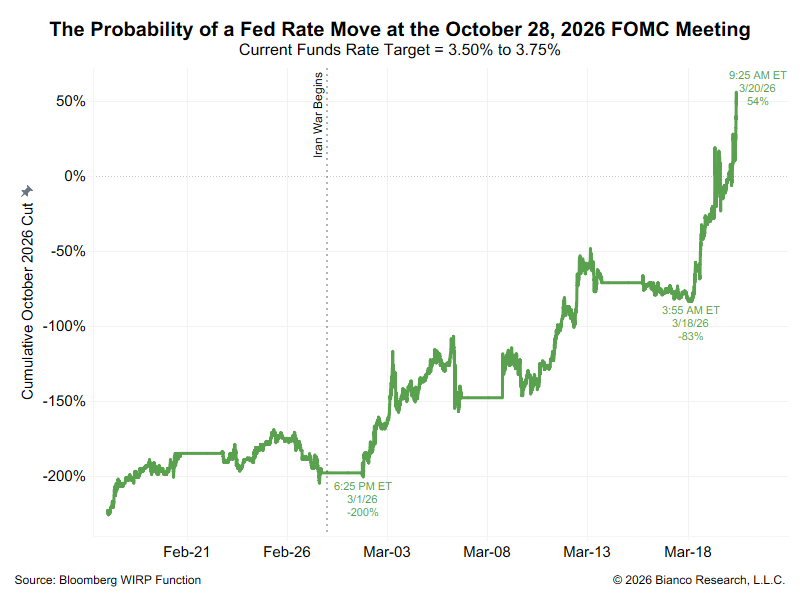

Three weeks ago, the day before the war started, WIRP said October was pricing in a 200% of a rate CUT (meaning two full cuts were priced in).

15 trading days later, it now has a 54% probability of a HIKE in October.

Orange = the forward Fed funds curve the day before the war. Blue = what the Fed dots say they expect to do. Green = forward curve today.

The gray arrow shows how expectations have moved in 15 days. This is a MASSIVE move over such a short period of time.

In the News

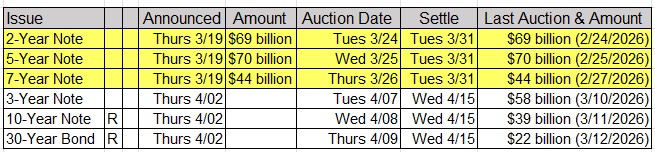

Upcoming US Treasury Supply

Upcoming Economic Releases & Fed Speak