Last week Chris Waller speech was called “The Case for Cutting Now.”

Waller: “My final reason to favor a cut now is that while the labor market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed, and other data suggest that the downside risks to the labor market have increased. With inflation near target and the upside risks to inflation limited, we should not wait until the labor market deteriorates before we cut the policy rate.”

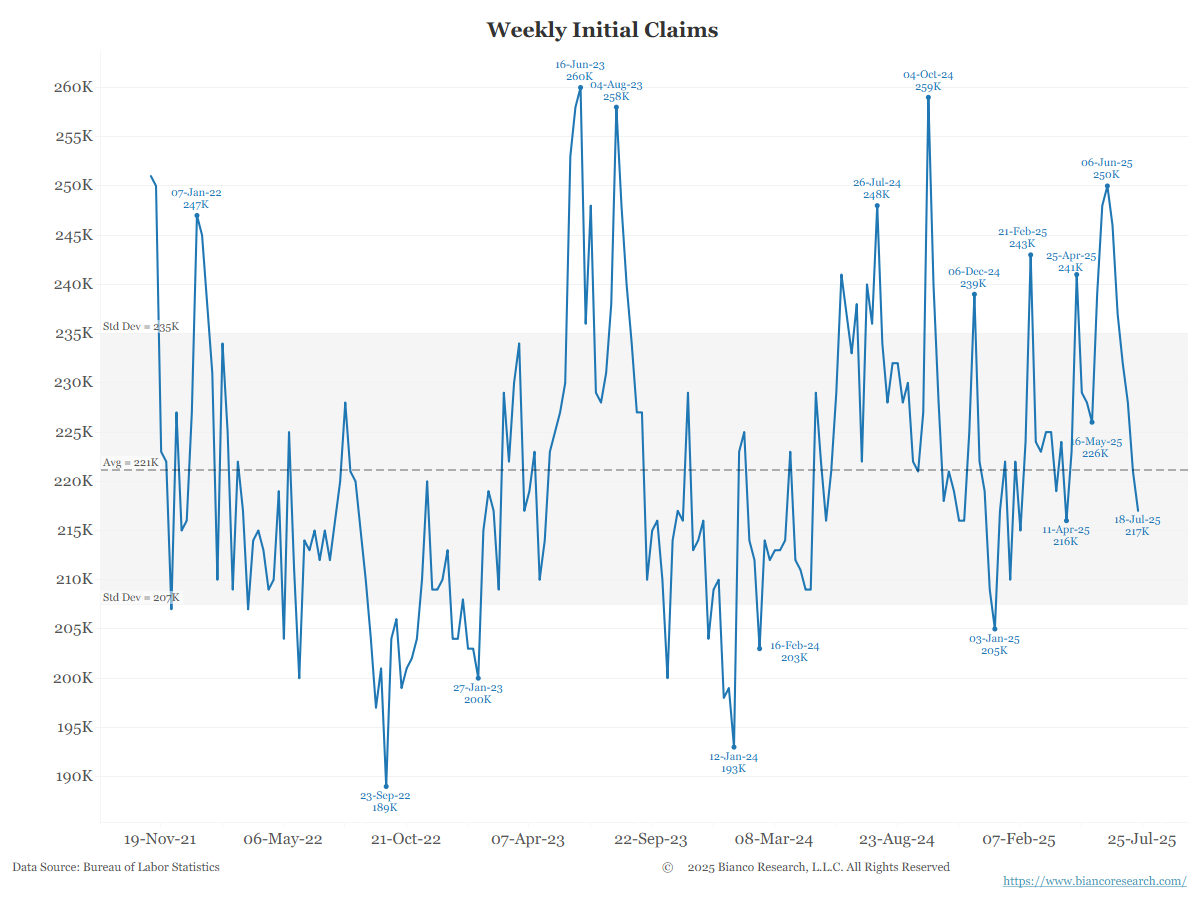

Claims are saying the opposite of Waller.

Waller again: “Looking across the soft and hard data, I get a picture of a labor market on the edge.”

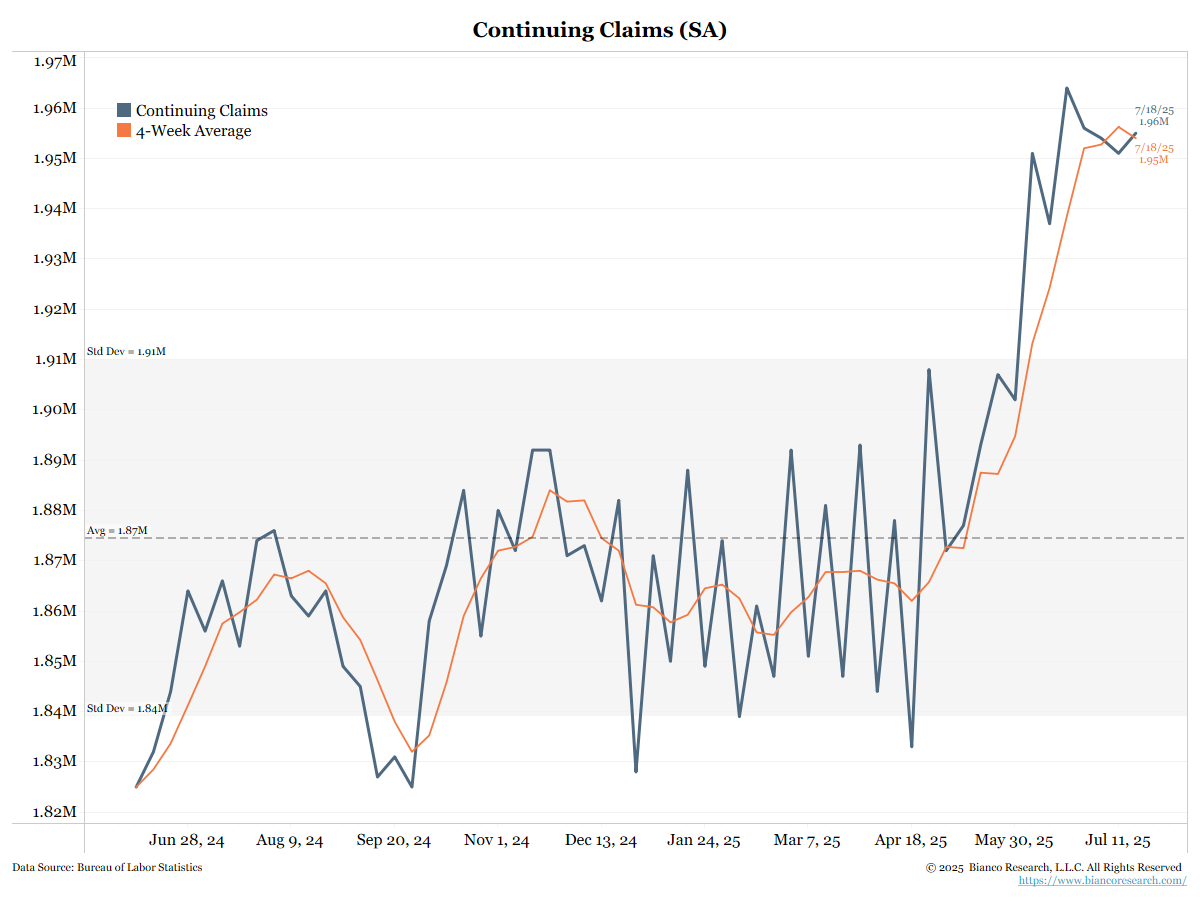

Even the data point that everyone was pointing to and worrying about, continuing claims, has stabilized at a level about 7,000 claimants higher than its recent average.

Having an extra 7,000 people on continuing claims is not a reason to cut rates, it will do nothing for them.

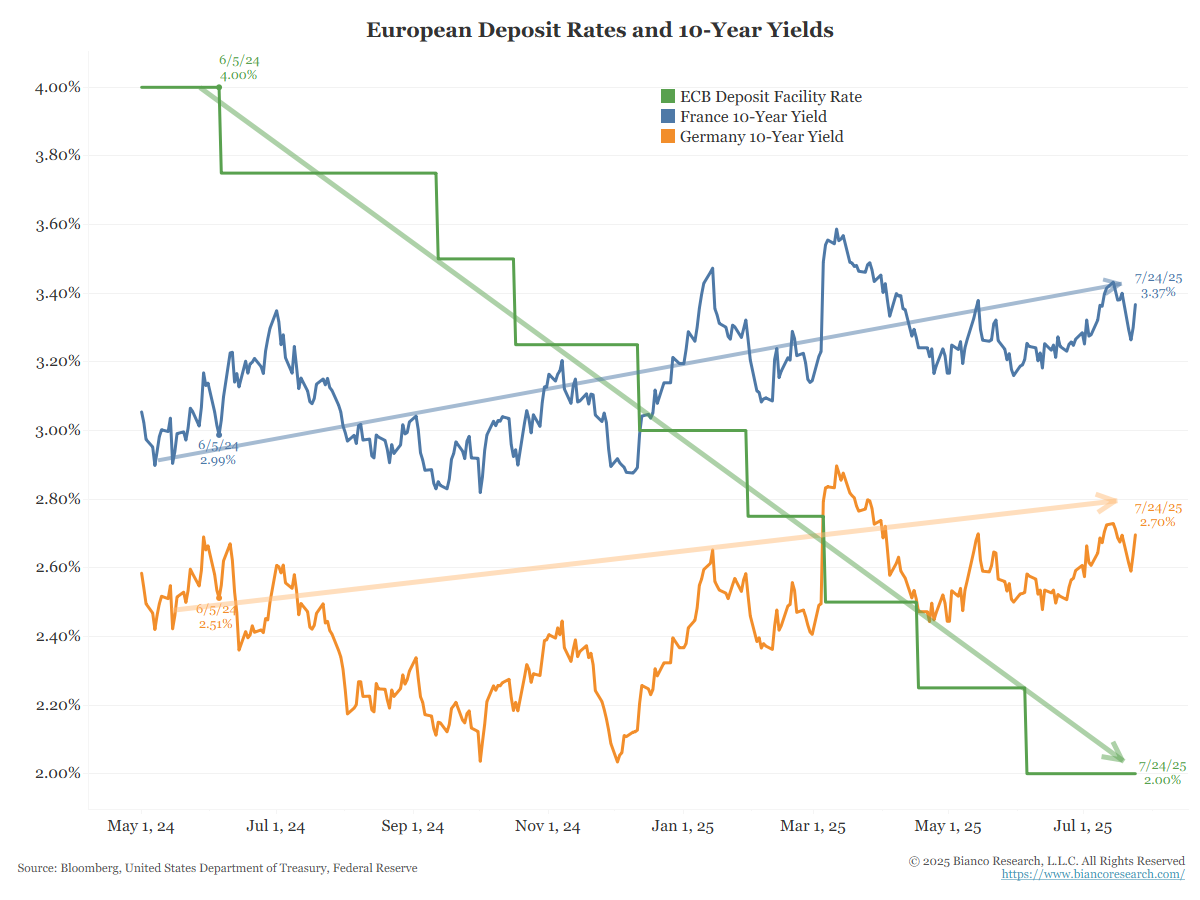

ECB has cut rates eight times over the last 13 months (green). During this period, the 10-year French (blue) and German (orange) yields have trended higher.

I’ve argued that this pattern is the market rejecting the central bank policy. It thinks it’s too easy, and it fears it will ignite more inflation.